Updated June 2026

What Is Liability Insurance Insurance?

Liability insurance is the foundation of every auto policy in Missouri. It pays for property damage and medical expenses you cause to others when you're at fault in an accident. Your liability policy includes two components: bodily injury coverage (the first two numbers in your limits) and property damage coverage (the third number). Missouri law requires you to carry at least $25,000 per person injured, $50,000 per accident for injuries, and $25,000 for property damage.

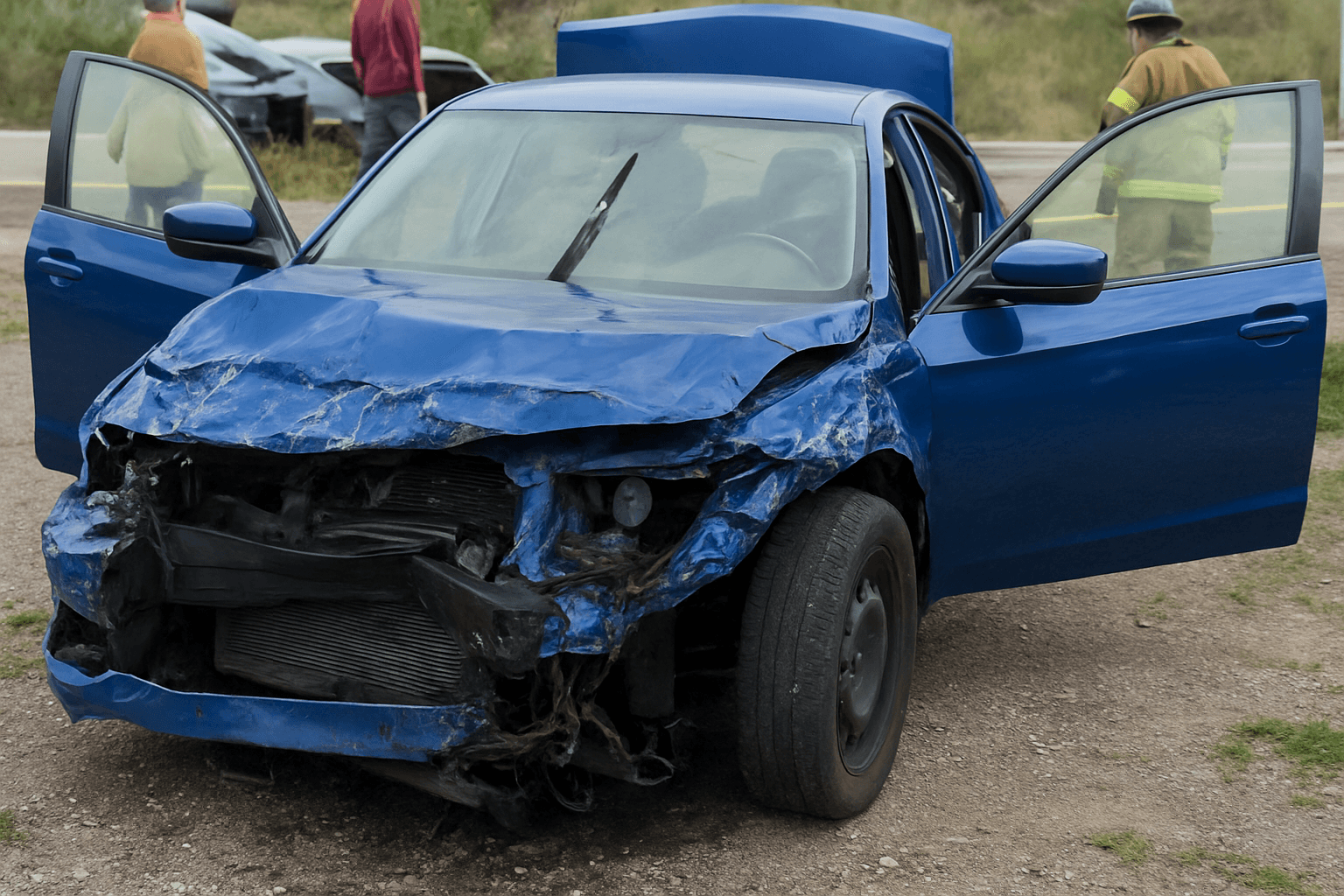

- You rear-end a stopped car at a red light. The other driver has $8,000 in vehicle damage and $4,500 in medical bills from a neck injury. Your liability coverage pays the full $12,500 to the other driver and their insurer. Your own vehicle damage—$3,200 to replace your front bumper and radiator—is not covered. If you only carry Missouri's minimum 25/50/25 limits, you're fully covered in this scenario because the total claim is under your $25,000 property damage limit and $25,000 per-person bodily injury limit.

- You run a stop sign and cause a three-car pileup. Two people in the first car have $40,000 and $35,000 in medical bills. The second car has $18,000 in damage. Your total liability exposure is $93,000. Missouri's minimum 25/50/25 coverage pays $50,000 maximum for all bodily injury ($25,000 to the first injured person, $25,000 to the second) and $25,000 for property damage. You are personally liable for the remaining $18,000 in unpaid claims. If you're reinstating after a suspension, this gap is why many drivers choose higher limits—minimum coverage protects your license reinstatement requirement but leaves you exposed to lawsuits.

- You borrow a friend's car and cause $9,000 in damage to another vehicle. You carry a non-owner liability policy because you're reinstating from a suspension and don't own a car. Your non-owner policy pays the $9,000 claim after your friend's insurance is exhausted. Non-owner policies provide secondary liability coverage—the vehicle owner's policy pays first, yours pays if their limits are exceeded. This structure satisfies Missouri's SR-22 insurance requirement without requiring you to own a vehicle.

Who Needs Liability Insurance Insurance?

Liability coverage is legally required for every Missouri driver reinstating from suspension, whether you own a vehicle or not. If your suspension was caused by DUI, excessive points, or driving uninsured, you must maintain continuous liability coverage for the full reinstatement period—typically three years for SR-22 filings. Non-owner liability policies satisfy this requirement if you don't currently own a car, and they're often the cheapest reinstatement option for suspended drivers who sold their vehicle or rely on borrowed cars.

If you're reinstating your license, carry at least Missouri's minimum 25/50/25 limits to satisfy state requirements. If you're reinstating after DUI or a serious violation and you have any assets—savings, property, wages subject to garnishment—increase your limits to 100/300/100 because minimum coverage leaves you personally liable for large claims. If you don't own a car, get a non-owner policy instead of trying to borrow someone else's insurance. If you're suspended but not actively reinstating, you can drop coverage entirely until you're ready to file for reinstatement.

How Much Does Liability Insurance Insurance Cost?

Liability-only coverage in Missouri typically costs $45–$85/month ($540–$1,020/year) for state minimum limits. Drivers reinstating after suspension or DUI often pay $75–$140/month due to high-risk classification. Non-owner policies cost $25–$50/month because they exclude vehicle damage coverage entirely.

- Suspension reason—DUI violations increase liability rates 80–150% compared to lapsed insurance suspensions

- SR-22 filing requirement—adds $15–$25 per six-month policy term as a carrier processing fee

- Liability limits selected—increasing from 25/50/25 to 100/300/100 typically adds $20–$35/month

- Driving record points—each at-fault accident in the past three years adds 15–30% to your base rate

- County of residence—urban Missouri counties like Jackson and St. Louis have 25–40% higher liability rates than rural counties due to accident frequency

- Coverage continuity—a lapse longer than 30 days during suspension reinstatement adds 20–50% to your quoted rate