Updated June 2026

What Is Uninsured Motorist Coverage Insurance?

Uninsured Motorist Coverage steps in when the at-fault driver has no insurance or insufficient coverage to pay your claim. It covers your medical expenses, lost wages, pain and suffering, and in some states your vehicle damage when the other driver can't or won't pay. You file the claim with your own insurance company, not the at-fault driver's nonexistent carrier. This coverage also applies to hit-and-run accidents where the other driver is never identified.

- A driver merges into your lane without looking, forces you into the guardrail, and drives off. You have $18,000 in medical bills and $9,000 in vehicle damage. If you carry Uninsured Motorist Bodily Injury with $25,000 per person limits and Uninsured Motorist Property Damage, your policy covers all medical expenses and the vehicle repair minus your collision deductible. Without this coverage, you pay the full $27,000 yourself.

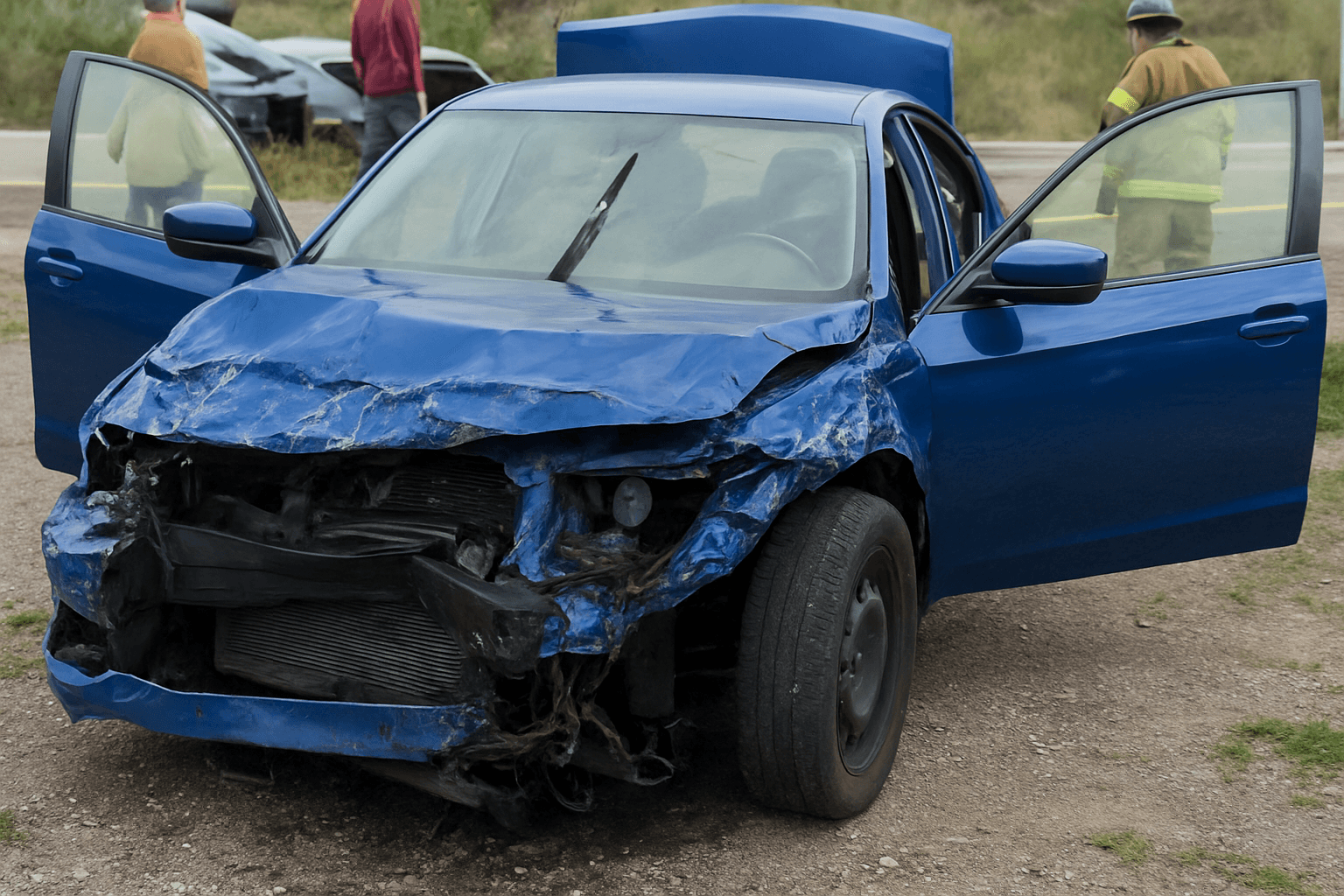

- You're stopped at a red light in St. Louis when an uninsured driver rear-ends you at 35 mph. You suffer whiplash and need 8 weeks of physical therapy totaling $6,200. The at-fault driver has no insurance and no assets. Your Uninsured Motorist Bodily Injury coverage pays the full $6,200. Without it, you sue the driver in small claims court and likely collect nothing because they can't pay.

- A driver runs a stop sign and T-bones your car. They carry Missouri's minimum $25,000 Bodily Injury limit, but your medical bills reach $42,000 after surgery. Their policy pays the $25,000 maximum. If you carry Underinsured Motorist Coverage with $50,000 limits, your policy pays the remaining $17,000. Without it, you're responsible for that gap unless you successfully sue the driver personally.

Who Needs Uninsured Motorist Coverage Insurance?

You need this coverage if your license is suspended and you're carrying SR-22 to meet reinstatement requirements — 12% of Missouri drivers are uninsured, and if one hits you while you're driving on a hardship or restricted license, a claim could derail your reinstatement timeline if you can't afford medical bills out of pocket. Drivers without health insurance benefit most because Uninsured Motorist Bodily Injury becomes your primary payer for accident-related medical treatment. If you're financing a vehicle and carry collision coverage, adding Uninsured Motorist Property Damage costs $3–$8/month and ensures you're not stuck with a repair bill and a car loan on a totaled vehicle.

Compare the annual premium to your health insurance deductible and out-of-pocket maximum. If your health plan has a $6,000 deductible and Uninsured Motorist Bodily Injury costs $12/month, you're paying $144/year to avoid a potential $6,000 bill if an uninsured driver hits you. If your deductible is $500 and you have $10,000 in savings, the value proposition weakens unless you're in a high-uninsured-driver county.

How Much Does Uninsured Motorist Coverage Insurance Cost?

Uninsured Motorist Coverage typically adds $8–$22 per month ($96–$264 annually) to your Missouri premium for $25,000/$50,000 Bodily Injury limits and $25,000 Property Damage.

- Your liability coverage limits — Uninsured Motorist limits cannot exceed your liability limits, so higher liability coverage opens access to higher UM limits and higher premiums.

- County uninsured driver rate — St. Louis City and counties with higher uninsured motorist rates see higher premiums because claim frequency is statistically higher.

- Your driving record — suspended license drivers pay 40–85% more for Uninsured Motorist Coverage because insurers price the coverage based on overall risk profile, not just the uninsured driver population.

- Whether you stack coverage — stacking multiplies your per-vehicle limits across all insured vehicles on the policy, which doubles or triples the premium but also the potential payout.

- Bundling with Underinsured Motorist Coverage — most Missouri carriers sell UM and UIM as a combined coverage, which costs less than buying each separately.